Credit Card Debt Nightmare: How 5.5% Interest Rates Will Impact You

Credit Card Debt Nightmare: How 5.5% Interest Rates Will Impact You

USA EDITION

The Federal Reserve's decision to maintain interest rates at 5.50% has significant implications for various aspects of the economy, including consumer behavior and debt management. Particularly, this decision plays a crucial role in shaping the landscape of credit card debt, which has been a pressing concern in recent years. According to the latest consumer debt data from the Federal Reserve Bank of New York, Americans’ total credit card balance reached $1.129 trillion in the fourth quarter of 2023, representing a notable increase from the previous quarter's record of $1.079 trillion. This surge in credit card debt underscores the importance of examining how the Fed's interest rate stance influences consumer borrowing and spending patterns.

Effect on Credit Card Debt: The Federal Reserve's decision to maintain interest rates at 5.50% has a direct impact on the cost of borrowing for consumers, including credit card holders. When the Fed keeps rates steady at this level, it implies that banks and financial institutions are less likely to adjust their prime rates, which are closely tied to credit card interest rates. Consequently, credit card APRs (Annual Percentage Rates) are likely to remain relatively high, making it more expensive for consumers to carry balances on their credit cards.

In practical terms, this means that individuals with existing credit card debt may find it harder to pay down their balances, as a larger portion of their payments goes towards interest rather than principal. Additionally, the high cost of borrowing may discourage some consumers from making new purchases on credit cards, leading to reduced consumer spending and potentially slower economic growth.

Furthermore, the sustained high level of credit card debt poses risks not only to individual financial stability but also to the broader economy. In the event of an economic downturn or unforeseen financial shocks, high levels of consumer debt could exacerbate financial distress for households and amplify the impact on overall economic activity.

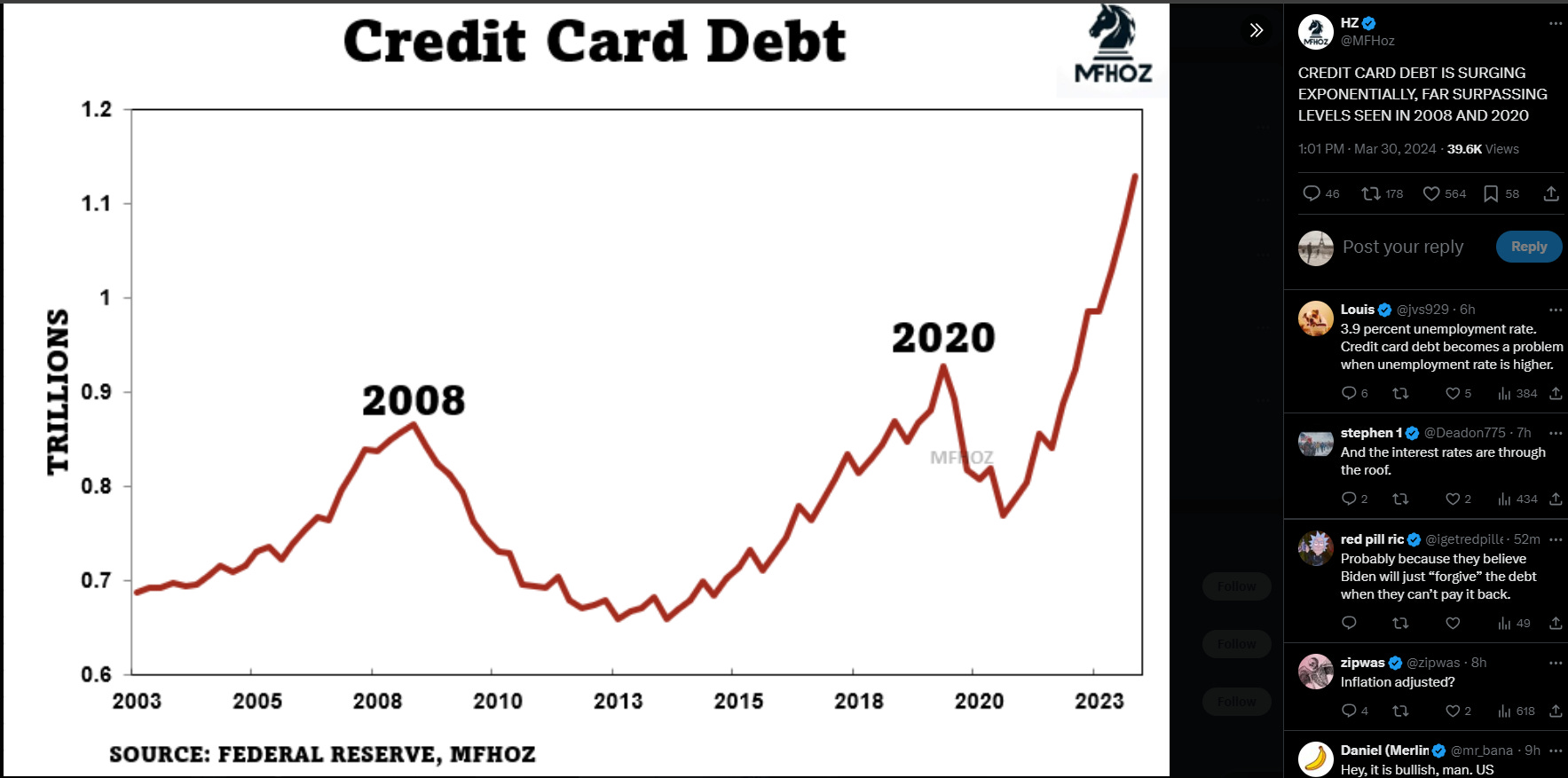

Quoting @ MFHoz on twitter and following the image:

The image confirms a troubling trend: credit card debt in the US is skyrocketing at an alarming rate. This surge is even steeper than the significant increases we saw in 2008 and 2020, according to data.

For reference, the financial crisis of 2008 and the economic hardship of 2020 were major events that caused many people to rely on credit cards. The fact that credit card debt is surpassing those levels highlights the severity of the current situation.

It's important to stay informed and make responsible financial decisions to navigate this challenge.

The image reveals a worrying trend: credit card debt in the US is climbing at an unprecedented pace. Data from the Federal Reserve Bank of New York shows that outstanding credit card balances reached a record high of $1.13 trillion in Q4 of 2023. This is significantly higher than the previous peak of $930 billion in Q4 of 2019, just before the pandemic.

For perspective, even during the economic downturns of 2008 and 2020, credit card debt didn't reach these levels. In fact, it dipped to $660 billion in Q1 of 2013 following the 2008 crisis. The current surge surpasses those historical peaks, highlighting the magnitude of the issue.

Here are two simple plans to help you manage debt, depending on the economic climate:

Plan A: Rates Stay the Same, Debt Increases (Worst Case Scenario)

Prioritize Needs vs. Wants: Track your spending and differentiate between needs (rent, groceries) and wants (dining out, subscriptions). Focus on reducing wants to free up cash for debt payments.

Negotiate Lower Rates: Contact your credit card companies and explain your situation. See if they'll lower your interest rate, especially if your credit score is good.

Explore Balance Transfer Offers: Look for 0% introductory APR balance transfer offers on other credit cards to consolidate your debt. This can buy you time to pay it down without accruing interest. Be aware of balance transfer fees and ensure you pay off the balance before the introductory period ends.

Increase Income: Consider a side hustle or explore ways to increase your income within your current job. Every additional dollar helps chip away at your debt.

Seek Free Credit Counseling: Non-profit credit counseling agencies offer free budgeting and debt management advice. They can help you negotiate with creditors and create a personalized repayment plan.

Plan B: Smooth Economic Recovery Next Year

Focus on Accelerated Payments: Use any additional income (like tax refunds or bonuses) towards your debt principal to pay it off faster.

Explore Debt Consolidation Loans: Compare rates and terms on consolidation loans to see if you can secure a lower interest rate than your current credit card debt.

Build an Emergency Fund: Aim for 3-6 months of living expenses in savings. This safety net can prevent relying on credit cards during unexpected financial emergencies.

Review Spending Habits: Reassess your needs and wants. With a potentially improving economy, re-evaluate your budget and aim to further reduce unnecessary spending.

Invest in Your Future: Once your debt is under control, consider investing in retirement savings or other financial goals.

Data and Resources:

Federal Reserve Bank of New York: Household Debt and Credit Report (https://www.newyorkfed.org/microeconomics/hhdc)

National Foundation for Credit Counseling: (https://www.nfcc.org/)

Remember: Consistency is key! Sticking to your plan, regardless of the economic scenario, will empower you to manage debt and achieve financial well-being.